For the last decade, many corporate IT organizations have been operating under the mantra of “doing (or delivering) more with less” – with a focus on reducing costs and increasing efficiency while still meeting higher business demand for IT services. And during this time, most – if not all – industry analyst firms have pointed to the fact that IT organizations continue to spend too much on their “keeping the lights on” activities versus innovation-based investments. With the former close to three times the latter.

However, as to whether this perpetual cycle of cost-cutting was the right approach for IT organizations to take is somewhat debatable. Not because there isn’t a potentially high level of IT spend “wastage” – there still is – but because potentially ill-informed decisions were being made around cost reduction. Decisions that could do more harm than good (thanks to the lack of granular cost understanding and the linkage of incurred costs to business value).

Better, Faster, Cheaper

Now the IT-mantra gods have moved the industry on – from “doing more with less” to “better, faster, cheaper.” Such that quality and speed are paramount, and with the improvements in these hopefully also reducing costs – particularly when automation is employed for quicker actions and reduced human errors.

In many ways, “better, faster, cheaper” is a far-superior mantra for IT, BUT it can still leave IT organizations in an IT-cost-based muddle – with the potential for improvement activities to be solely focused on quality and speed gains.

These, of course, aren’t bad things to focus on, it’s just that this continues to potentially leave IT organizations with a lack of insight into:

What individual IT services cost

Why IT services cost what they do, and

The service-related opportunities to save money without a noticeable effect on quality (and speed)

Financial Management – One of ITIL’s “Poor Relation” Capabilities

For those who like numbers, ITIL 2011 has 26 processes and four functions – it’s way more than ITIL v2’s ten processes and the IT service desk. But at least two-thirds of these 26 processes are somewhat “unloved” and not used by the “average” IT organization – with financial management being one (of these).

As to why, your guess is as good as mine – with the most obvious answer being that organizations have, to date, been able to survive without out it, and potentially despite the pain that its absence causes. Ten years ago, another excuse would have been the lack of tools and methods for measuring IT costs and value; and then for presenting them from an organizational perspective. But that excuse no longer holds.

Yet, despite that persistent pressure on most IT organizations to “do more with less,” there’s still significant work to be done to improve the insight into, and understanding of, IT costs. This might sound like an “negative,” but it’s in fact a massive opportunity for organizations to improve service delivery and support on a number of levels – from freeing funds for greater investments in innovation, through gain competitive advantage, to better demonstrating the value of IT.

Now is a great time to take control of what IT costs and to adjust that expenditure accordingly (in line with business wants and needs).

Understanding IT Costs at a Granular Level – Service Costing

Service costing is the key to IT financial management success. And it starts with the creation of a framework, or a model, within which all known costs can be captured and allocated to important “entities.”

These could be specific IT services, customers, locations, or other activities. And only by building this IT cost model can an IT organization truly start to understand: the costs incurred, how these costs are driven, how the costs are “consumed” by IT services (or other entities such as business units), and the value delivered by IT services versus the consumed costs.

In a service-based IT cost model, costs are attributed to the service, or services, that cause them to be incurred. There will be direct costs, those clearly attributable to a single service, and indirect costs, those incurred on behalf of two or more services that need to be apportioned to multiple services in an equitable manner.

Using such as cost model allows an IT organization to gain multiple insights into IT costs, for example:

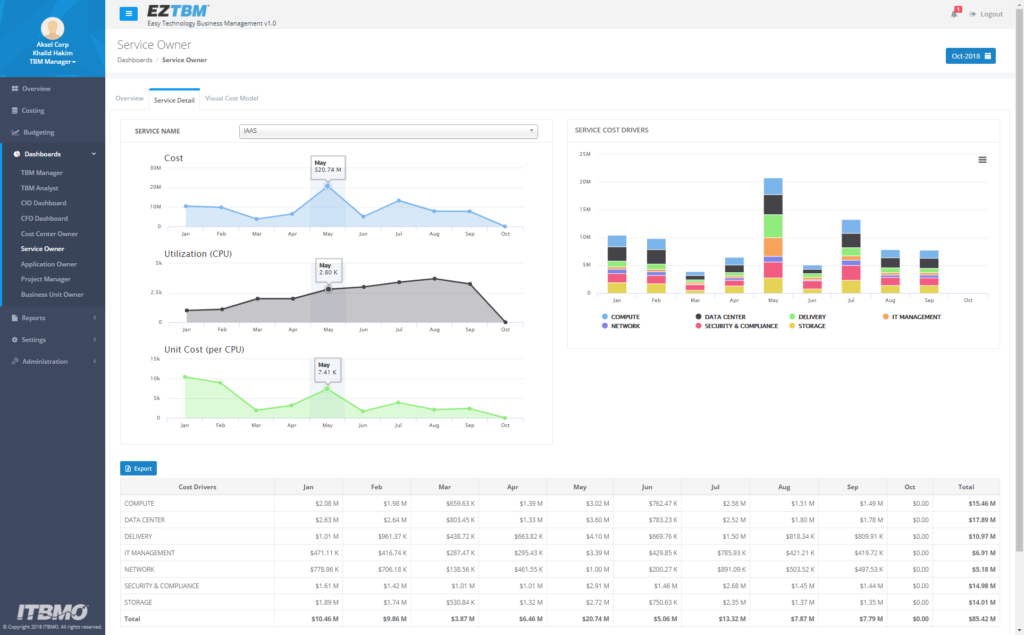

- A unit cost for individual IT services, e.g. the corporate email service (please see the image below). This can then be used for comparison against industry benchmarks or alternative, commercially available, services. It can also be used in customer-based conversations about cost and value.

- The cost drivers for individual IT services. With the information then facilitating decisions around changes to operations, such as migrating workloads and services to the cloud. Or changes to service levels that might offer up significant cost savings for a minimal reduction in quality. Or, conversely, demonstrating the dramatic increase in costs associated with a proposed upping of service levels.

- Cost-based trends can be monitored to understand the performance gain or loss. Plus, capacity-based trends can be understood from a cost perspective. Or what-if scenarios created based on probable future changes to the IT infrastructure (and third-party service consumption) and the associated impact on costs.

Example Service and Unit Costs Over Time

Granular Cost-Based Metrics Can Be Employed to Drive Improvement and Communicate Successes

The outputs of service costing can become powerful performance metrics. However, there’s no one-size-fits-all set of IT cost metrics – each organization will have a different view on which (metrics) are best-suited to measuring and demonstrating their performance across perspectives such as cost efficiency, IT spend/investment mix, and business-value delivery. And such metrics, trended over time, will help identify both past achievement and future opportunities for service (and cost) improvement.

Example metrics, that employ service-costing-based granularity of insight, include:

- PC and laptop, or data-center-related, total cost of ownership (TCO)

The ability to trend these metrics over time, such as in the example below, will allow your IT organization to better understand the direction of both operational and financial performance, plus the positive impact of your improvement initiatives (or, conversely, the opportunities to improve).

Cost Performance Trends

It’s important to stress here, though, that while such metrics might not seem like “rocket science,” there’s definitely a need for “finance science” to get the level of granularity into the costs, and their associated costs drivers, required to report them accurately; and then to make informed business decisions about future operations and spend.

So, how well do you understand your IT costs? Contact ITBMO to help you create, enhance, and operationalize your service-based cost model in a more simplified manner.